Checklist For Choosing the Best Payment Orchestration Platform

Digital payments have skyrocketed in recent years, making a robust payment infrastructure critical for businesses….

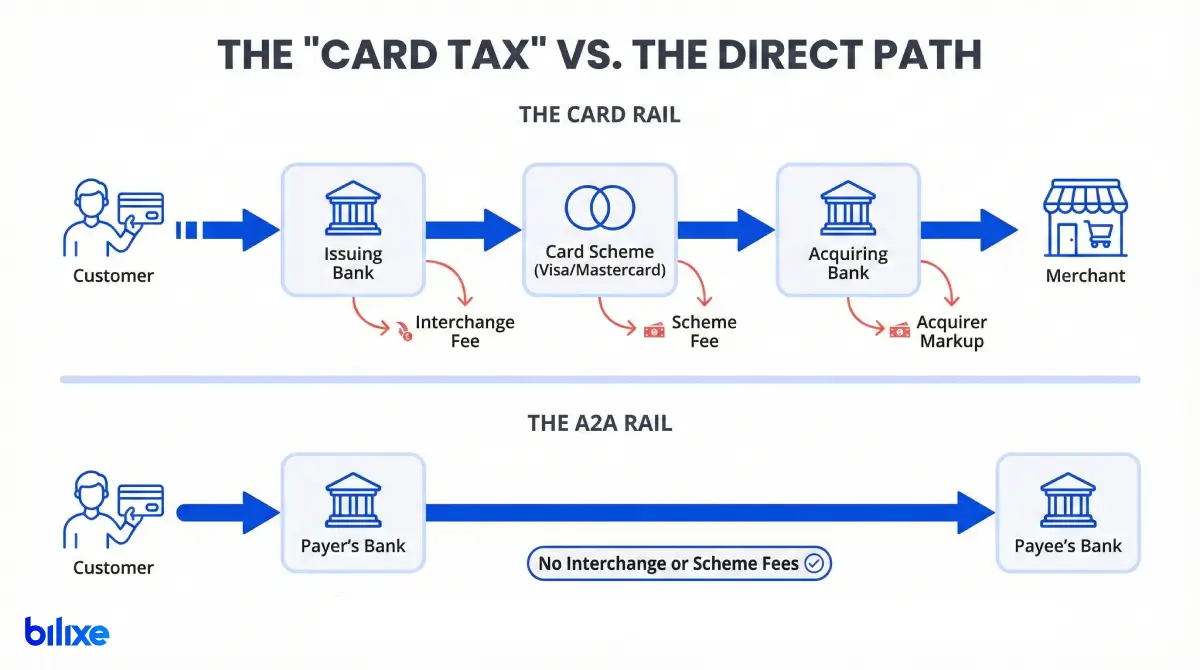

The global infrastructure for value exchange is undergoing a significant transformation, more impactful than the introduction of the magnetic stripe or chip card. For decades, commerce has primarily relied on a model established in the 1950s: the credit card network. This system involves a complicated structure with issuing banks, acquiring banks, and centralized card schemes.

A new approach is emerging that challenges this dominance through regulatory changes and technological advancements. This report offers an in-depth look at open banking and A2A payments. It provides modern merchants with a practical guide to navigate this shift.

The global open banking market was valued at about USD 31.61 billion in 2024 and is expected to grow to USD 135.17 billion by 2030. This indicates a Compound Annual Growth Rate (CAGR) of 27.6% during this period, showing a strong and steady increase in adoption. At the same time, the number of Account-to-Account (A2A) payments is projected to rise from 60 billion transactions in 2024 to over 186 billion by 2029.

This growth is not gradual but exponential, driven by the development of instant payment systems and widespread mobile banking usage.

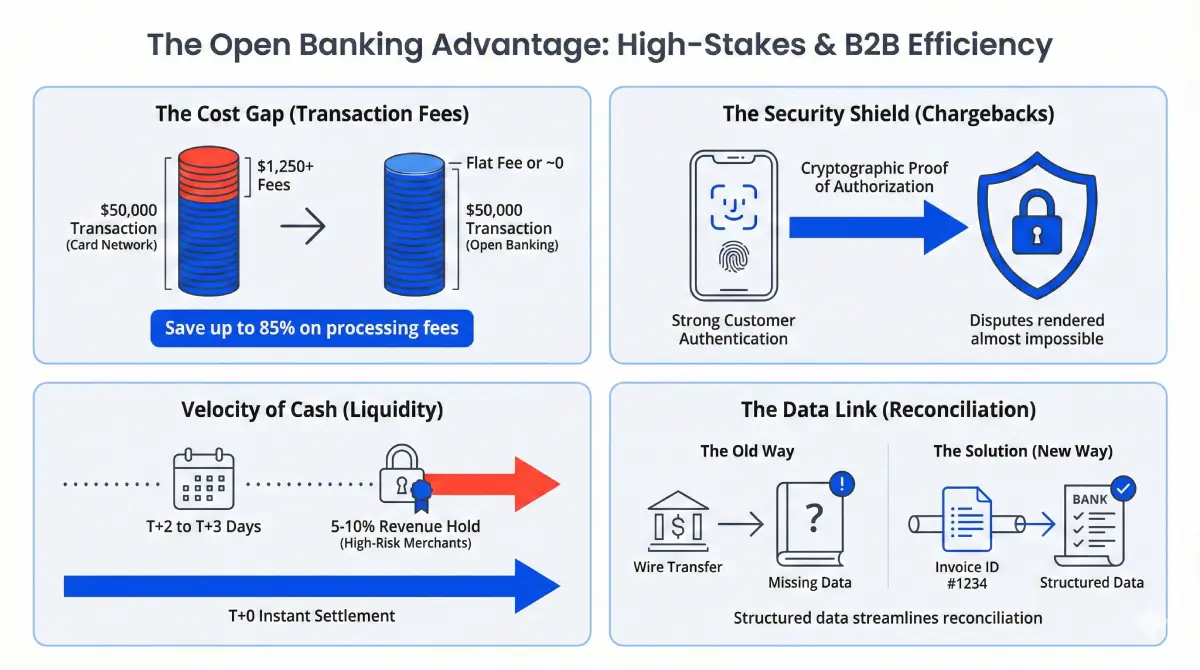

Merchants are increasingly focused on payment methods that provide “instant liquidity”. In the traditional card system, it typically takes two to three days to settle a transaction. In contrast, modern A2A solutions use real-time gross settlement (RTGS) systems to transfer funds in seconds.

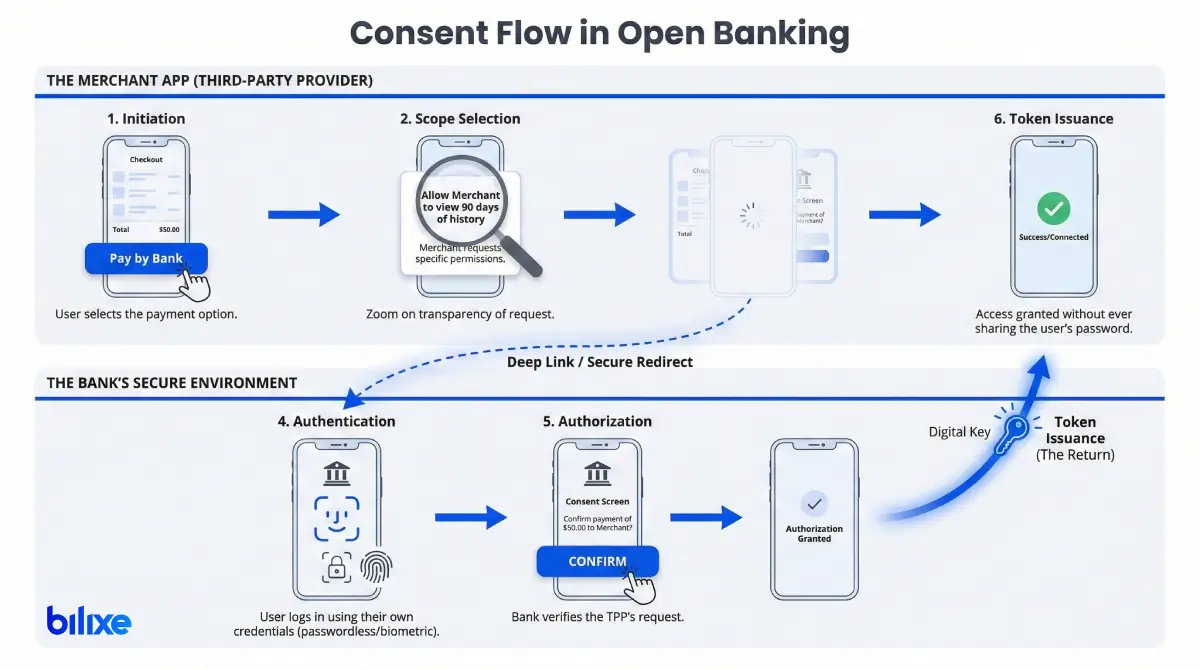

Open banking is the governance and data layer. It refers to the rules and technology that allow banks to share customer financial data with regulated Third-Party Providers (TPPs). It is the “pipe” through which information flows.

Open banking standards clarify how a third party securely identifies itself to a bank, how a customer gives consent, and how data is structured during transmission.

The technology driving open banking is the Application Programming Interface (API). APIs act as the language and gateway between the bank\s internal systems and the TPP.

In open banking, consent is the key governance mechanism. It is the “opt-in” step that legitimizes data sharing. The consent process typically follows a standard pattern known as the “Redirect Flow” or “App-to-App Flow”.

This process ensures high levels of transparency:

Account-to-Account (A2A) Payments are the execution layer. This term represents the actual transfer of money from the payer’s bank account to the payee’s bank account without using card networks like Visa or Mastercard.

While A2A payments have existed for years as manual transfers or ACH batches, modern A2A payments stand out due to their integration with open banking APIs. This allows for payment initiation directly within a merchant’s checkout process, providing an experience similar to card payments but with the advantages of direct credit transfer.

To understand A2A efficiency, we must examine the cost structure of the card model. When a customer swipes a card, a complex chain of intermediaries activates, each taking a share of the transaction.

The combined effect of these layers results in the Merchant Discount Rate (MDR), which can cost businesses between 1.5% and 3.5% of gross revenue.

A2A payments avoid this whole structure. Because the payment is a direct transfer between banks, there are no interchange or scheme fees. The cost is usually just a low flat fee or a minimal percentage with a cap.

For a high-value transaction of $5,000, a 2.5% card fee leads to a $125 cost. An A2A fee might be capped at $5.00. This means a 96% reduction in payment processing costs for that transaction.

Push Payments vs. Pull Payments

Instant Payment Rails

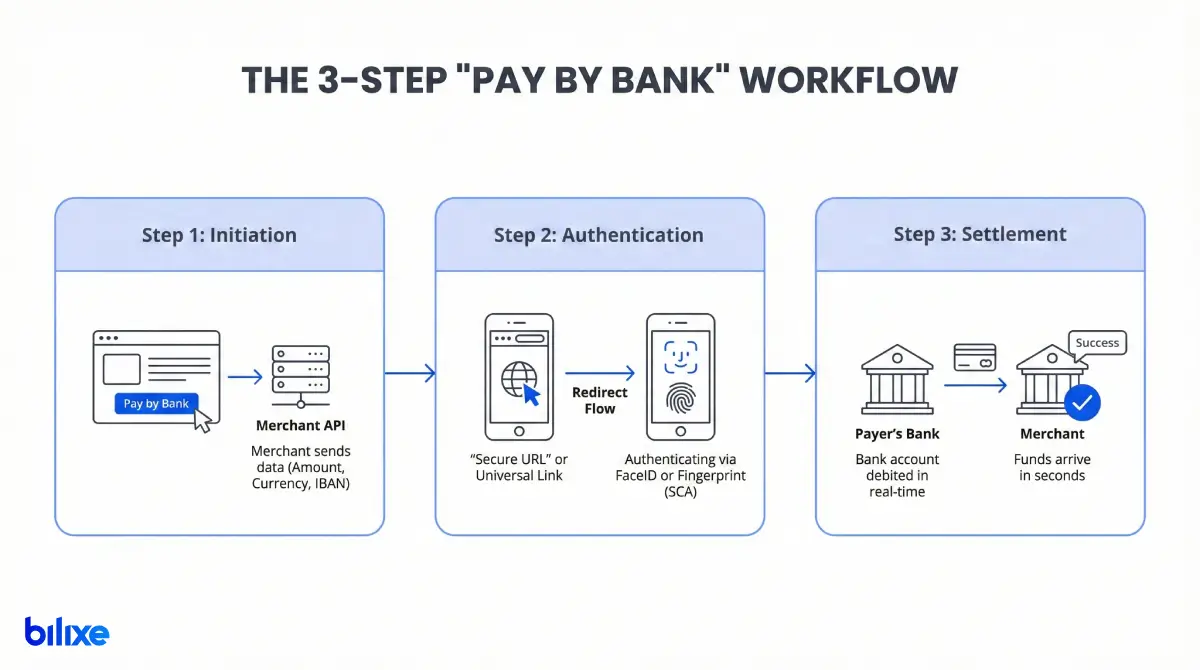

For merchants integrating these solutions, understanding the technical workflow is crucial.

The process starts at checkout. Instead of entering card details, the customer chooses “Pay by Bank”. The merchant’s server sends information to the PISP’s API, including the amount, currency, creditor account (IBAN), and a unique reference ID for tracking.

The merchant redirects the customer to their banking app via a secure URL. On mobile devices, this uses “Universal Links” or “App Links” to open the banking app directly, bypassing the browser. The user authenticates using Strong Customer Authentication (SCA), often through face scans or fingerprints. They review the payment details and confirm.

Once confirmed, the bank debits the user’s account in real time and sends a payment instruction to the clearing system. The funds arrive in the merchant’s account within seconds. The merchant receives a success notification, marks the order as “Paid”, and releases the goods. This entire process can take less than 10 seconds.

While the advantages of open banking apply to all merchants, they are especially transformative for specific categories like high-risk industries (iGaming, Forex, Crypto) and B2B businesses:

We are moving from a system that relies on expensive intermediaries and outdated card infrastructure to one based on direct connections, secure cryptography, and instant settlements. This is not just a small improvement. It represents a significant change in how efficiently global commerce operates.

Merchants face increasing risks if they do nothing. To navigate this environment, merchants should use resources like the bilixe. Bilixe offers a searchable database of payment service providers (PSPs). Whether a business needs high-risk processing, B2B reconciliation, or specific regional instant payment options, bilixe helps compare and connect with suitable partners.

The foundation for a quicker, cheaper, and safer financial system is built. It is now up to modern merchants to connect.

Recommended Articles

Digital payments have skyrocketed in recent years, making a robust payment infrastructure critical for businesses….

The checkout page is the key moment for any online business. It is the point…

What Is a Payment Gateway? A payment gateway is a technology that enables merchants to…

Find the Best Payment Service Provider for Your Business